Monday, June 02, 2008

Analysing The World Food & Fuel Situation, It's Impact and Avenues For Growth

Let’s face it, the global economy is reeling; it is tottering under the pressure of two most pressing demands from humanity; Food & Fuel. With the fissures between the developed and the developing worlds closing on, scampering for every last bit of resource available is never before. Lifestyle has been a major catalyst behind; developed world led by USA has been trying hard to maintain its wasteful living standards, on the other, developing countries like India and China, egged on by their new found riches are creating additional pressures on world supplies of food & fuel. If you think the present scenario is short term, here is a small did you know for you:

-

The Food and Agricultural Organisation (FAO) warned that the present stock of world food would last only for 57 days [1]

-

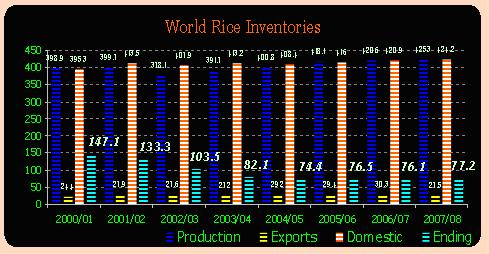

World inventories of rice have fallen by nearly 50 % from a record high of 147.1 million tonnes in 2000/01 [2]

-

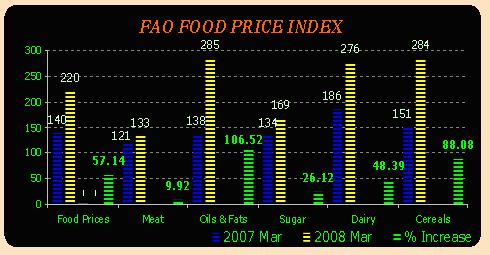

Between March 07 & 08, the world food prices have jumped 57 %, Cereals, which are major consumable of world’s poor notched an increase of 88% [3]

And, above all,

-

The world decreased poverty by about 0.68 % annually starting from 1984. But at the current rate of annual poverty increase induced by rising food inflation the entire global 22 year improvement in impoverishment will be completely erased by 2012.[4]

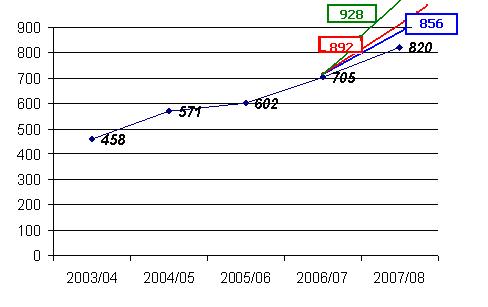

4 years, just four years to throw us back to the levels of poverty as witnessed in 1984. Shocking as it is, it is true as well. The heat is on and the projections maddening. Rice, a staple for about 3 billion people around the globe, a big majority of which are from the developing world, now has the potential to rake the biggest humanitarian catastrophe, food riots. It is estimated that the world will need an additional 50 million tons of rice a year in the years to 2015, about 9 percent more than current production. Of this, Asia will account for 58% and sub-Saharan Africa - 21%.[5] Just enough to cause food riots and hoarding campaigns.

The rising food prices, though is a recent phenomena, and presumably (what one might think of as the first underlying cause) India and China are to blame. This is only a fraction of what the realityholds. The existing price trends reflect not only that shortfall in production as opposed to consumption; they also reflect an attempt to rebuild the stocks, thereby putting even greater pressure on demand relative to supply.[6] Further, the present scenario is simply not a by-product of demand supply interactions. Another factor that did not get sufficient coverage is the rising attractiveness of the commodities sector to the investors. The recent financial market turmoil has exerted enough pressures on investors to look for avenues with higher returns. Commodities with high expected rates of return in contrast to money market instruments have attracted investors. Speculative trading in agricultural commodities has grown dramatically. Several big investment banks have launched agricultural commodity index funds, as they look for new areas to make profits in following the credit crunch. The result has been enormous fluctuations in market prices that do not appear to relate to changes in fundamentals such as supply and demand. Four years ago $10-15bn was invested in agricultural commodities funds - now that figure is more than $150bn. Wall Street investment funds own 40% of US wheat futures and more than one fifth of US corn futures.

Given the situation at hand, the leading lights of the world have now a task to burn the midnight oil. From Oil, which traded a $ 33 a barrel just about a year back, is all set to leapfrog the $150 threshold, after which it is supposed to stabilise. During last year, the escalating oil prices pushed up the cost of food production dramatically, as a result, fertiliser is up more than 70%, fuel for tractors and farm machinery is up 30%, pesticides, which depend on oil, are rising too[7]. Two countries majorly are behind this, China & USA. India, which is the world’s fifth largest consumer of energy accounting for 3.9% of world’s annual energy consumption is heavily skewed towards coal (about 50%) and oil & gas (about 42%), with hydro (6%) and renewables (1 – 1.5%) contributing for much less.

In a period of just about 10 years, China has increased its oil consumption by 86%. From 4.2 million barrels a day in 1997 to 7.8 in 2007, and projections now point to 8 million bpd in 2008. While the domestic supplies remained more or less static at about 3 million bpd, China today imports nearly 4 million barrels a day. On the other hand, USA consumes 21 million bpd and imports 13 million bpd. It is US consumption which sets the pace in international oil markets. Given the Chinese competition, both USA & China are competing for access to overseas supplies, thereby edging up prices. Of course, shrinking oil output from such key producers as Mexico, Russia and Venezuela; internal violence in Iraq and Nigeria; refinery inadequacies in the U.S. and elsewhere; speculative stockpiling by global oil brokers are other factors to blame.[8]

Analyzing Food & Fuel Price Shocks[9]

World Bank’s food price index climbed 57.5% in the first quarter of 2008 relative to the corresponding figure a year ago. At the same time, energy prices have also been on an upswing, with the World Bank’s oil price index growing by 66.5% in the first quarter of 2008. This cascades to developing Asian economies’ growth and inflation prospects. The rise in oil prices is critical in analyzing food price increases since fertilizer prices, which are highly dependent on petroleum and natural gas prices, move in tandem with energy prices.

Since food carries a large weight in the CPI of many of the Asian economies, global food price increases translate to higher prices in developing Asia. Considering both the Global oil price increase along with the world food price increases, it is estimated that

-

The regional inflation would rise by 2.38 percentage points in 2008. Consequently,

-

The private consumption is expected to shrink by 1.38 percentage point

-

In order to prevent inflation from spiralling uncontrollably, the government would raise interest rates, according to ADB estimates interest rates in developing Asia would go up by 2.79 percentage points, and as a result

-

GDP growth in developing Asia is estimated to shrink by 1.41 percentage points in 2008 and in 2009 by 4.15 percentage points

Fiscal Impact of the Rising Food and Oil Prices

Given the poverty considerations in many developing countries, governments run food safety programmes, these programmes, heavily reliant on subsidies from the government aim at providing subsidized food to consumers and providing subsidized fertiliser to farmers. Rising food and oil prices are directly adding to the food subsidies in food importing developing countries and in other countries the governments are under pressure to increase procurement prices in order to give right price signals to farmers and generate a larger supply response. In the context of India, assuming the government has to raise the procurement prices by 10, 20 and 30 percent respectively, it is estimated that the budgetary cost of this higher procurement prices would be in the tune of 4%, 9% and 13% respectively.

Impact on Procurement Prices in India

The Way Forward

The present stalemate, though long term, is not without a solution. It is highly recognised that the developing world, now, commands an impressive growth prospects. Agriculture, which is fraught with rudimentary production practices in such regions, is one such sector that can not only support local economy but also help improve world food situation. It has been estimated that the World Food Program has a shortfall of about $ 755 million in its funding and given the slowdown in the world economy, pegging such a gap is nearly impossible. On the other hand, there has been a rise in the number of countries such as United Arab Emirates, Norway, Saudia Arabia, Kuwait, Singapore, China and Russia which owing to their oil exporters’ status lends them an ability to maintain Sovereign Wealth Funds in G-8 economies. These countries have nearly $2 Trillion tucked in sovereign wealth funds for investment abroad and as much as 35 countries, now manage $3 Trillion through such funds. Even if, say 1 % of this amount is invested in areas where agriculture needs support in form of R&D for raising productivity, infrastructure development and modernisation of farming practices etc much of the world’s problem can be solved. Africa is one such region.

[1] The Daily Star: Managing Food Crisis

[2] Reuters

[3] FAO

[4] HuffingtonPost: Bird Flu, Rice and Gas Guzzling

[5] Bloomberg: Rice May Withstand Climate Change, Top Scientist Says (Update2)

[6] Asian Development Bank [ADB]

[7] Guardian: FAQ: The five factors that are driving up costs

[8] LATimes: The U.S. and China are over a barrel

[9] Food Prices Inflation in Developing Asia; ADB 2008

No comments yet